Non‑Payment: Customer Failed to Pay – Can Your Business Sue in the UK?

Customer failed to pay your invoice? Learn how the UK small claims court helps businesses recover unpaid debts and how Casecraft can support your non-payment claim.

What Counts as Non‑Payment in Business?

Non‑payment happens when a client refuses or fails to pay what they owe under a contract. For small firms, it usually falls into three patterns:

- Customer not paying invoices – the client ignores payment reminders or simply refuses to pay. Law views this as a contractual breach (an example of “breach of contract” in the UK for small business owners) and allows you to take action.

- Partial payment or long delays – the buyer pays part of the invoice but withholds the balance, or constantly delays payment. Even partial delays can be treated as late payment under the Late Payment of Commercial Debts (Interest) Act 1998.

- Invoice disputes are used to avoid paying; some customers raise spurious disputes about the quality of work or goods to avoid payment. Unless there is a genuine problem, refusing payment is still non‑payment.

Non-payment of invoices harms cash flow for small businesses, forcing you to spend time chasing unpaid bills and adding stress. As part of small business debt recovery, if a customer fails to pay an invoice, UK legislation gives you the right to claim compensation for unpaid invoices and to recover statutory interest and fixed recovery costs.

Common Scenarios of Customer Non‑Payment

Non‑payment affects freelancers, sole traders and SMEs across many sectors. Some typical situations are:

- Freelancers not paid for completed work – designers, copywriters and consultants often face clients who enjoy the finished product and then fail to pay. Because the work is intangible, it can be harder to enforce payment without written contracts, so use deposits and clear milestones to mitigate the risk and, if necessary, be ready to enforce a court judgment.

- Suppliers of goods or services receiving no settlement – small manufacturers or service providers deliver goods/services, but the customer fails to pay the invoice. They may claim the goods were “faulty” without evidence or simply ignore communications. This constitutes non‑payment and is recoverable through the courts.

- False excuses for withholding payment – a client might dispute an invoice to delay payment or hope you will give up. If there is no genuine dispute (e.g., they received the correct goods or services), this is still non‑payment. Keep evidence of delivery and correspondence.

Your Legal Rights Under UK Law

Late Payment of Commercial Debts (Interest) Act 1998

- Charge statutory interest: When another business is late paying for goods or services, you can charge statutory interest of 8% plus the Bank of England base rate. This rule applies to business‑to‑business contracts. For example, if you’re owed £1,000 and the base rate is 0.5%, the annual statutory interest is £85.

- Debt recovery costs: In addition to interest, you can charge a fixed sum for debt‑recovery costs based on the value of the debt. GOV.UK explains that you can charge £40 for debts up to £999.99, £70 for debts between £1,000 and £9,999.99, and £100 for debts of £10,000 or more. You may also recover reasonable costs incurred while chasing the debt.

These rights are implied into commercial contracts by statute. Even if your contract is silent about interest or recovery costs, the Act entitles you to claim them. This helps deter late payers and compensates you for the time value of money.

Supply of Goods and Services Act 1982

The 1982 Act implies terms into contracts for services. If the contract doesn’t specify a price, the Act states that the customer must pay a reasonable charge. What is “reasonable” depends on the circumstances. This protects suppliers when a customer tries to avoid payment by arguing that no price was agreed upon.

Civil Procedure Rules and Small‑Claims Track

Part 27 of the Civil Procedure Rules (CPR) sets out the small‑claims track. It explains that the small‑claims track is the normal track for claims with a financial value of no more than £10,000. Claims for personal injuries have lower limits, but for most commercial disputes about unpaid invoices, the £10,000 cap applies. The rules limit the legal costs recoverable from the losing party and make the process quicker and less formal.

Because small‑claims cases are designed to be accessible, you generally cannot recover the cost of solicitors. This is why platforms like CaseCraft.AI exist: they help small businesses navigate the procedure without incurring high legal fees.

Steps to Take Before Suing a Customer

The courts expect parties to try to resolve disputes before issuing proceedings. Pre‑action protocols are formal steps you must follow. Citizens Advice explains that you should send a letter before claim (also called a “letter before action”) to the debtor. Here is a step‑by‑step approach:

Send a reminder invoice

A polite reminder often prompts payment. Include details of the due date, amount owed and any interest accruing.

Issue a final notice

If the reminder fails, send a stronger letter warning the client you will take legal action if the debt is not paid, setting out your commercial debt recovery position. Refer to the Late Payment of Commercial Debts (Interest) Act 1998 and specify the statutory interest and fixed recovery costs you will claim.

Draft a letter before claim

This letter should include your name and address, a summary of what happened, the amount owed and how you calculated it, a deadline for reply (usually 14 days) and a warning that you will start court proceedings. Citizens Advice emphasises that you should refer to the pre‑action protocol under the Civil Procedure Rules and warn of potential sanctions if the debtor fails to comply.

Offer mediation

Mention that you are willing to try mediation or alternative dispute resolution. Mediation can save time and money.

Keep records

Preserve all contracts, invoices, emails and delivery receipts. Evidence is vital if the case goes to court. Ask the Post Office for proof of postage when sending your letter.

Using Small‑Claims Court for Non‑Payment

Is Your Claim Suitable?

The small‑claims track generally covers claims up to £10,000. This limit includes interest but does not include court fees. Claims for personal injury or housing disrepair have lower thresholds. If your claim exceeds £10,000, it will be allocated to the fast or multi‑track, and legal costs become recoverable. For most unpaid invoices, however, the small‑claims track is appropriate.

What You Can Claim

In a small‑claims non‑payment dispute, you can typically recover:

- The principal debt is the amount of the unpaid invoice.

- Statutory interest – 8% plus the Bank of England base rate. You calculate this daily and add it to your claim.

- Fixed debt‑recovery costs – £40, £70 or £100 depending on the debt value, plus reasonable additional costs.

- Court fees – the court fee you pay to issue the claim and, if necessary, the hearing fee.

You cannot generally recover solicitor’s fees, because costs are limited, many businesses dealing with unpaid business invoices handle the process themselves or use CaseCraft.AI.

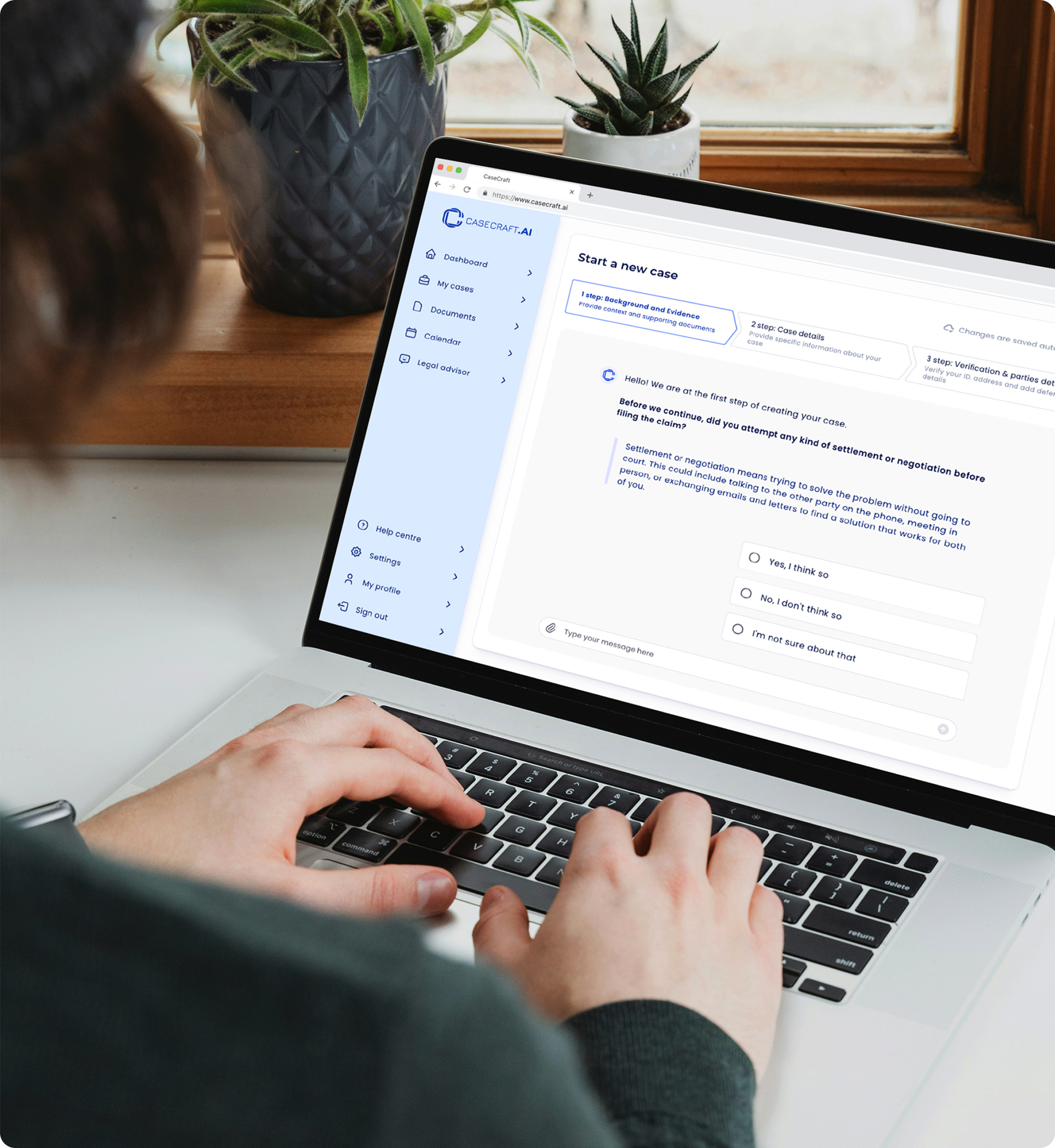

Filing the Claim: CaseCraft.AI and Civil Money Claims

To file a small‑claims case in England and Wales, you can:

- Submit the N1 paper claim form – download and print an N1 form, complete it and send it with the court fee to the County Court Money Claims Centre.

- Use the online services – CaseCraft.AI prepares and lodges your claim through the government’s online money-claims system.. For straightforward claims under £10,000, the newer online route applies; you must be over 18, have a UK address, and you can’t use it for personal injury or Consumer Credit Act matters.

During the online process, you will enter details of the claim, upload evidence and pay the fee. If the defendant disputes the claim, the case proceeds to a hearing in a local county court.

What Happens at the Hearing

Small‑claims hearings are informal compared with higher‑court trials. Each party explains their case, presents evidence and answers questions from the judge. The judge’s decision (called a “judgment”) will state how much the defendant must pay and the deadline for payment. If you win and the debtor still refuses to pay, you can enforce the judgment by applying for methods such as a warrant of control, attachment of earnings or a charging order.

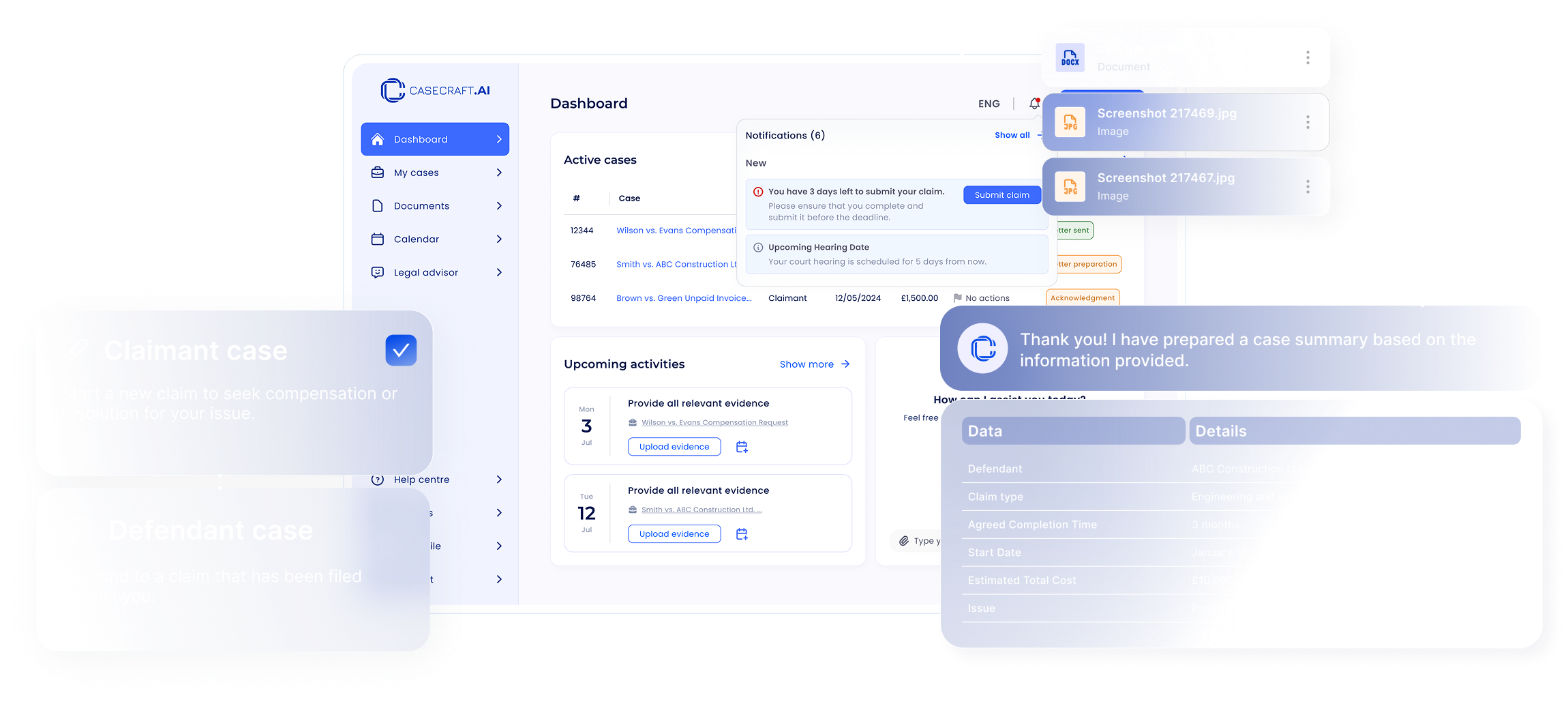

How CaseCraft.AI Helps with Non‑Payment Claims

CaseCraft.AI is a UK-based platform that uses AI to streamline the small-claims process for any small claims non-payment dispute. The service charges a £15 onboarding fee and a success fee of 15% of the amount recovered. Key features include:

- Reviewing contracts and invoices – the platform checks your documentation to ensure your claim is strong.

- Drafting formal demand letters – CaseCraft.AI can prepare letters that comply with the pre‑action protocols and Late Payment legislation, including interest and debt‑recovery costs.

- Preparing and filing the claim – the AI assists in completing the Civil Money Claims forms and submitting them online. It guides users step‑by‑step, reducing errors that lead to default judgments.

- Arranging mediation – Casecraft helps clients book the free mediation session offered by HM Courts & Tribunals Service.

- Court representation and negotiation – if the case proceeds to a hearing, the platform provides guidance and may connect you with legal professionals for complex questions.

By automating these tasks, CaseCraft.AI makes the small-claims process accessible to small businesses that cannot afford solicitors and need to sue a customer for non-payment. CaseCraft.AI aims to reduce these failures by guiding claimants through each step and ensuring compliance with court rules.

Why Choose CaseCraft.AI for Debt Recovery

- Specialised in B2B and B2C non‑payment – CaseCraft.AI focuses solely on small-claims disputes and debt recovery, small claims work; its AI has been trained on numerous scenarios, so it can handle both business-to-business and consumer cases.

- Cost‑effective and transparent – you only pay a £15 processing fee and a 15% success fee if you win. This is far cheaper than hiring solicitors, whose fees are not recoverable in the small‑claims track.

- Time‑saving and stress‑reducing – automated reminders, document generation and claim submission free you from administrative work.

- End‑to‑end support – from drafting the letter before claim to filing the case and arranging mediation, Casecraft supports you throughout the process.

- Experienced team – founded by legal professionals and technology experts, CaseCraft.AI combines legal knowledge with AI to offer legal help for non-payment claim support. The co-founders include experienced solicitors and technologists.

Preventing Future Non‑Payment Issues

Recovering unpaid invoices is costly, so prevention is better than a cure. Put steps in place now to strengthen any future invoice claim:

- Use written contracts – always have a contract that specifies the price, payment terms, interest for late payment and dispute resolution. Written agreements make it easier to prove your claim.

- Set clear payment terms and late fees – state your payment period (e.g., 30 days) and note that interest under the Late Payment Act will accrue after that. Include fixed debt‑recovery costs.

- Request deposits or staged payments – for large projects, ask for an advance or milestone payments. This reduces the risk of large unpaid balances.

- Perform credit checks – research a new client’s creditworthiness. Refuse or limit credit if there are red flags.

- Automate invoicing and reminders – use accounting software to send invoices promptly and chase late payments automatically.

Real-Life Examples of Non‑Payment Claims We Handle

1. Customer Refusing to Pay for Delivered Goods

A small furniture maker delivered bespoke tables to a retailer. The retailer claimed the tables were “unsellable” but offered no evidence and refused to pay £4,500. The maker sent a letter before claim, claiming the debt, interest and £70 recovery cost. When the retailer still refused, the maker filed a claim using CaseCraft.AI. At the hearing, the judge accepted delivery evidence and awarded judgment for the debt, interest and costs. With CaseCraft.AI’s help, the process was efficient, and the maker recovered funds within weeks.

2. The client is ignoring multiple invoice reminders

A freelance web developer completed a project for a start‑up. Despite multiple reminders, the client ignored a £2,200 invoice. The developer used Casecraft to generate a final notice and a letter before claim. After no reply, she filed an MCOL claim. The client admitted the debt and paid the full amount plus interest and costs before the hearing. Casecraft’s automated guidance ensured the claim complied with pre‑action protocols, discouraging the client from disputing it.

3. Dispute over services used as an excuse for non‑payment

A consultancy provided marketing services under a contract without a fixed price. After receiving the final report, the client refused to pay, arguing that no fee had been agreed upon. Under the Supply of Goods and Services Act 1982, there is an implied term that the client must pay a reasonable charge. The consultant sent a letter before the claim, citing the Act and the Late Payment legislation. With CaseCraft.AI’s support, the consultant filed a small‑claims case. The court ordered the client to pay the consultant’s reasonable fee, statutory interest and recovery costs.

Friendly Asked Questions

What exactly counts as “non-payment” and when can I act?

If a person or business owes you money for goods or services and doesn’t pay, you can bring a county court money claim (“small claims court”) after you’ve tried to resolve it and followed basic pre-action steps. You can apply online or by post.

Can I add interest and late-payment charges?

Yes. For business-to-business debts, you can add statutory interest at 8% + the Bank of England base rate (unless your contract sets a different rate) and claim a fixed recovery fee (£40/£70/£100 depending on the debt size), plus reasonable recovery costs.

Is my matter a small claim, and what’s the limit?

In England & Wales, the small claims track is normally for money claims up to £10,000, with special lower limits for personal injury and housing disrepair.

What must I do before suing?

Courts expect “pre-action conduct”: send a letter before claim with enough detail and time to respond, and consider mediation. Skipping this can harm your case.

Do I need a solicitor, and will I get legal costs back?

Small claims are designed to be low-cost and accessible; recoverable legal costs are strictly limited, so many businesses handle them without instructing solicitors. (That’s why structured support and automation are valuable.)

Case Study: Claim for recovery of Unpaid Fees

The parties agreed by email in January 2024 to a 10% brokerage fee, which became due in November 2024 when the client secured an office. The defendant disputed the fee and later breached a settlement plan agreed in January 2025, leaving £5,000 unpaid. A claim was filed for breach of contract and non-payment of the agreed fee, including statutory interest. Shortly after the claim was issued, the parties reached a new settlement, and the defendant paid £5,158.22 in full and final resolution.

CaseCraft.AI supports all common types of small money claims

From unpaid invoices to cancelled orders and ignored reminders late or missing payments can damage your cash flow and business stability. CaseCraft.AI helps UK businesses recover debts through the small claims process quickly and cost-effectively, without complex legal steps or hidden fees.

Don’t Wait – Get Started Today!

Take the first step toward a faster, easier small claims process with CaseCraft.AI.