Explore 2025/26 UK student loan repayment rules: thresholds, interest rates, plans, and how CaseCraft.AI helps resolve small disputes.

For many students, a loan that they take out is needed for university attendance. Tuition fees are covered, and assistance for living costs exists. Higher education is thus more accessible to all. But the reality is that when you lend money to a student, you don’t give it freely; you agree financially, along with any contract, terms change over time.

Many graduates will therefore see lower deductions alongside new responsibilities with the changes. This guide currently explains student loan repayment rules in the UK, highlights differences between repayment plans, and outlines what happens when things don’t go to plan. It draws only from official data obtained in 2025/26.

Student loans differ from commercial credit agreements. When you take out a loan, you enter into a formal contract with the Secretary of State for Education in England or the Welsh Ministers in Wales. The Student Loans Company (SLC) administers these loans on behalf of the government.

Repayments are collected through the tax system, and both the repayment threshold and the interest rate depend on your plan and the current year. Because mismanaging a student loan can lead to penalties or legal action, understanding the rules is critical. CaseCraft.AI specialises in small claims, so we know how important it is to handle disputes over‑payments efficiently.

Your Student Loan Agreement

Your loan contract is governed by regulations that set out the terms and conditions of borrowing. In England, your contract is with the Secretary of State for Education; in Wales, it is with the Welsh Ministers. The SLC acts as the agent for these authorities and is responsible for paying out borrowings, adding interest, collecting repayments and managing your account.

These rules can change. Repayment thresholds and interest are updated annually, with new thresholds taking effect from 6 April 2025. For 2025/26, the Retail Price Index (RPI) used to set interest was 4.3% (applied from 1 September 2024 to 31 August 2025). From 1 September 2025, new rates will apply, calculated using the March 2025 RPI.

You can find more detailed guidance in the 2025 to 2026 Student and Postgraduate Loan Deduction Tables published by HMRC here, and in the official Student Loans: Terms and Conditions 2025 to 2026 guide issued by the Department for Education here.

Roles and Responsibilities in Student Loan Repayment

Understanding the division of responsibilities will help you navigate the system. The SLC manages your account, adds interest and applies repayments collected through the tax system. HM Revenue & Customs (HMRC) collects loan repayments from employees through the Pay As You Earn (PAYE) system and passes this information to SLC. Employers must deduct the correct amount if your income exceeds the relevant threshold and receive guidance from HMRC about which plan applies.

Declare loans properly

If you’re self‑employed, you repay through the Self Assessment system. When you complete your annual tax return, you must declare your student loan, and HMRC will calculate the repayment due. Those who work overseas for more than three months must contact the SLC before leaving the UK. Instead of PAYE, SLC will set a monthly repayment based on your overseas income and convert it into sterling. Failing to provide income details can lead to a fixed charge or even court action.

Key Responsibilities in Managing Your Loan

- Provide accurate information. Giving false or incomplete information when applying can result in immediate repayment or a penalty.

- Update personal details promptly. Before you leave the UK, inform the SLC if you change your name, address, bank account, university or course.

- Submit your National Insurance number. SLC cannot process your loan application without it.

- Tell SLC about changes in employment. Switching from employment to self‑employment, taking a break from study or withdrawing from your course can all affect your repayment status.

- Comply with overseas obligations. If you work or travel abroad for more than three months, arrange repayments directly with SLC.

Failing to meet these responsibilities can lead to higher interest (RPI plus 3% for Plan 2 loans), fixed repayments when you’re overseas or legal action. Keeping your details current also protects you from over-payments.

Repayment Plans Explained

The plan you’re on determines your repayment threshold, the percentage of income you repay and how interest is applied. For 2025/26, the thresholds were increased by around 4.3%. Here are the main plans:

- Plan 1 (pre‑2012 loans in England and Wales) – Repay 9% of income above £26,065. Interest is the RPI of the previous March, or 1% above the highest base rate of a nominated group of banks (Bank Base Rate), whichever is lower. Any balance is written off 25 years after liability begins, or when you reach age 65.

- Plan 2 (post‑2012 loans in England and Wales) – Repayments start in April after finishing your course. You repay 9% of earnings above £28,470 a year. Interest is RPI plus 3% while studying, and then ranges from RPI to RPI + 3% depending on your income after study. The debt is cancelled 30 years after you become liable.

£28,470 or less: 4.3% (RPI only)

£28,471 to £51,244: 4.3% plus up to 3% (sliding scale)

£51,245 or more: 7.3% (RPI plus 3%)

- Plan 4 (Scottish undergraduate loans) – Repay 9% of income above £32,745. Interest is 1% above the Bank of England base rate, or RPI if lower. The interest rate is set on 1 September each year, although it can change during the year. Any balance is written off after 30 years.

- Plan 5 (loans for courses starting on or after 1 August 2023) – Plan 5 applies to courses starting on or after 1 August 2023. The repayment threshold is £25,000, rising with inflation from April 2027. You repay 9% of your income over that figure. Interest is RPI only, and balances are written off after 40 years.

- Postgraduate loans (Plan 3) – Postgraduate loans require repayment of 6% of income above £21,000. Interest is RPI plus 3%, and the debt is wiped after 30 years.

These thresholds determine when repayments start and how much of your income goes towards clearing the debt. Repayments are based on income, not the amount borrowed, so you will never repay more than a percentage of your earnings above the threshold. If your income dips below the relevant threshold, deductions stop automatically

How Repayments Work

Repayments are collected through the UK tax system unless you’re working overseas. If you’re employed, your employer deducts loan repayments from your salary alongside tax and National Insurance. HMRC passes the information to SLC, which updates your account and calculates interest. Self‑employed borrowers include student loan repayments in their annual Self Assessment return; failure to submit a return or pay on time can result in interest and penalties.

Monthly deductions are calculated based on each pay period. If you earn more in a particular month, you may pay a larger amount that month, even if your annual income is below the threshold. If you leave the UK for more than three months, notify the SLC. It will set repayments based on your overseas income; failing to provide details can result in a fixed repayment or legal action.

Student borrowings are not a debt for life. Each plan includes a cancellation provision, and loans are written off after 25, 30 or 40 years, depending on the plan or at age 65 for older Plan 1 loans. Death, permanent disability or administrative errors can also lead to cancellation. You may make extra payments at any time to reduce the principal balance, but voluntary payments do not reduce the statutory deductions collected via PAYE or Self Assessment. To minimise the risk of over‑payment when your balance is nearly cleared, SLC recommends switching to Direct Debit near the end of your repayment term. If you do overpay, refunds are available through your online account and interest on over‑payments is capped at 60 days.

Complaints, Appeals and Dispute Resolution

Automation has reduced errors, but problems still occur. If you believe the SLC has made a mistake or provided poor service, you can raise a complaint by phone, email or post and request an independent review if you are still unhappy. You can also appeal certain decisions, such as a refusal to award funding or an incorrect assessment. Appeals must be made using the official form on the government’s student finance website.

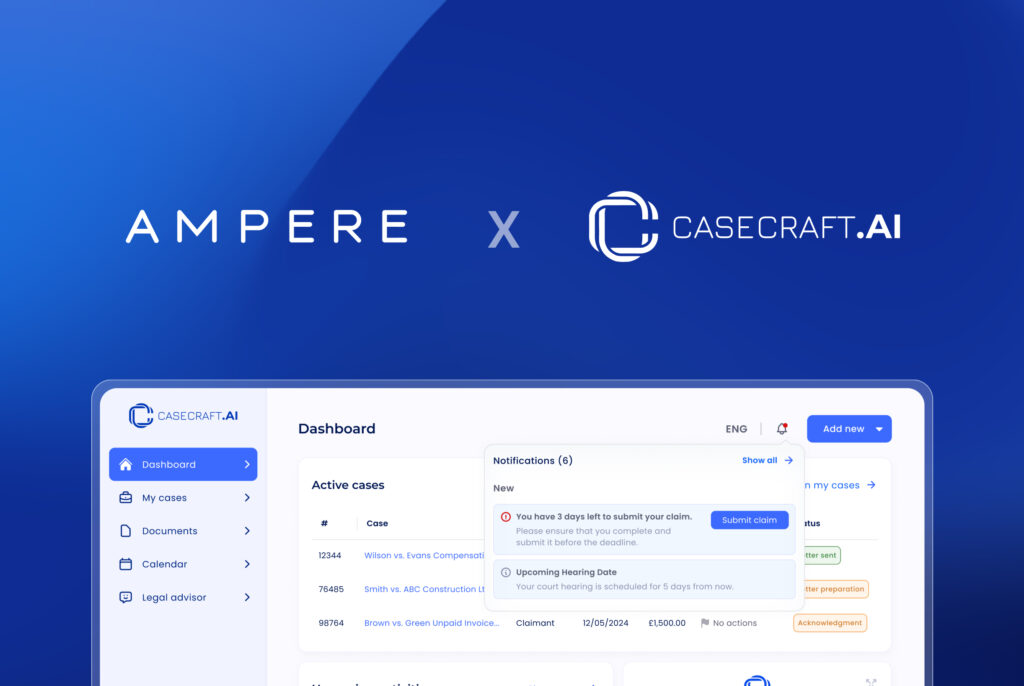

For smaller disputes, like overpayments or administrative errors, it can feel daunting if someone pursues a formal complaint. Here is the place where CaseCraft.AI can help; it automates the small-claims process as well as prepares compliant documents. It follows deadlines, and that simplifies getting your due money without costly legal help.

Bringing It All Together: How CaseCraft.AI Fits In

Comprehension of the student loan repayment rules enables proactive debt management. Disputes can sometimes arise in the event that you were charged with deductions after the time your loan was cleared. You might face different issues if your overseas work involved overpayment. These small amounts need to be resolved, as CaseCraft.AI can surely help.

CaseCraft.AI makes low‑value civil claims simpler in England and Wales since it automates documents, tracks due dates and ensures rule following. The service, which legal experts developed, charges a success fee along with a modest processing fee. A user‑friendly dashboard lets you upload evidence, monitor progress and receive smart alerts. These features are invaluable when recovering a small sum from an overpayment or administrative error on your student loan, and most such disputes fall within the £10,000 small‑claims limit.

To use CaseCraft.AI for a student loan dispute, gather supporting documents, such as payslips or correspondence, and submit your claim through the platform. The AI helps produce court‑ready documents and track deadlines. For disputes exceeding the small‑claims limit or involving complex legal issues, seek specialist advice.

The 2025/26 rules show the UK government adjusting the balance between affordability for graduates and cost recovery for taxpayers: thresholds have risen, but interest remains linked to inflation. By understanding your plan, keeping your details current and managing repayments proactively, including using Direct Debit near the end of your term, you can keep your student loan manageable. Should a small dispute arise, CaseCraft.AI offers an efficient way to pursue a claim within the small‑claims limit.

FAQ: Student Loan Repayment: 2025/26

How are student loan repayments calculated in the UK?

Repayments are income-based. You repay a percentage of earnings above your plan’s threshold through PAYE or Self Assessment. If your income falls below that threshold, deductions stop automatically until your earnings rise again.

What are the main differences between Plan 1, Plan 2, Plan 4 and Plan 5 loans?

Each plan has its own threshold, interest rate and write-off period. Plan 1 and 4 have higher thresholds, Plan 2 has variable interest up to RPI + 3%, and Plan 5 uses a lower threshold with RPI-only interest and a 40-year write-off.

What happens if I move overseas with a UK student loan?

You must notify the SLC before leaving. Repayments switch from PAYE to an income-based overseas schedule. Failure to provide income details can trigger fixed monthly charges or legal enforcement.

Can CaseCraft.AI help with student loan overpayment disputes?

Yes. Small disputes, often involving over-deductions or administrative errors, fall within the small-claims limit. CaseCraft.AI prepares compliant documents, organises evidence and tracks deadlines, making it easier to recover money owed.