1. Winning doesn’t guarantee payment. After judgment, the debtor normally has 14 days to pay. If they don’t, you can enforce a money judgment using bailiffs, wage deductions or other court orders. Interest at 8% per year accrues until the debt is paid.

2. Choose the right enforcement tool. Bailiffs (warrants of control), high court writs, attachment of earnings orders, charging orders, and third‑party debt orders are the main options. Each has its own fee and suitability depending on the debtor’s assets.

3. Keep records and act within six years. You can enforce a CCJ for six years. After that, you must ask the court for permission to proceed. Always keep evidence of communications, payments, and enforcement attempts in case you need to prove your actions later.

Introduction

Winning a claim in the United Kingdom’s small‑claims court feels like the end of the story – at last, the judge has agreed you are owed money and has made it official. Yet a judgment does not magically put cash in your bank account. A county court judgment (CCJ) is a legal order compelling the defendant to pay, but it is still up to you, the successful claimant, to make sure payment is actually collected. If the debtor ignores the judgment or fails to meet a payment plan, you must take the next step and enforce the order.

This in‑depth guide is written for individuals and small businesses who have recently won a small claim and now want to understand exactly what happens after you win a small claim. It explains the post‑judgment process in plain language, outlines the tools available to enforce a CCJ and shows how digital assistants like CaseCraft.AI can help you stay organised.

The article follows a step‑by‑step structure, so you’ll learn how long you must wait before taking action, when interest starts adding up, what it costs to involve bailiffs and what to do if the debtor still refuses to pay.

Step 1: Understanding the County Court Judgment (CCJ)

After a successful hearing, the court issues a county court judgment. This is a binding order stating how much money the defendant must pay and by when. In plain terms, a CCJ is a formal recognition that someone owes you money, and the court supports your claim. The judgment becomes enforceable immediately, defining the relationship between the judgment debtor and creditor, but it still gives the debtor a short period to pay. Typical outcomes are:

- Immediate payment: The judge may order payment in full within a fixed number of days (often 14).

- Instalment plan: If the defendant proves they cannot pay at once, the court may set a monthly instalment schedule. Instalments are still part of the judgment and can be enforced if missed.

- Non‑payment: If the defendant ignores the order or stops paying instalments, you will need to enforce the judgment.

What happens after you win a small claim? Once you win, the court issues a CCJ. The debtor usually has 14 days to pay. If a payment order is missed, you can enforce the judgment through bailiffs, wage deductions, property charges or third‑party debt orders. Interest at 8% per year accumulates on unpaid amounts.

Failing to comply with a CCJ has consequences beyond your case. Every judgment is recorded on the Register of Judgments, Orders and Fines and appears on the defendant’s credit file. Paying in full within 30 days can remove the entry; otherwise, the record stays for six years. Because lenders often check this register, unpaid judgments severely damage credit scores and can make it harder for the debtor to obtain loans or mortgages.

Why Small Claims Have Limits?

The small-claims track is designed for low-value disputes, freeing up court time and enabling simpler, quicker procedures.

As of 2025, the general small claims limit is £10,000 for most cases. However, personal injury claims have different limits depending on the type of accident:

- Personal injury (non-road traffic): £1,000 for injury damages

- Road traffic accidents (vulnerable road users – pedestrians, cyclists, motorcyclists, horse riders): £1,000 for injury damages

- Road traffic accidents (other, such as car drivers/passengers): £5,000 for injury damages under the RTA Small Claims Protocol

- Housing disrepair: £1,000 for estimated repair costs

The overall claim value (including property damage, expenses, etc.) can still reach £10,000, but the injury element is separately capped as above.”

Claims exceeding these thresholds are moved to the fast track or multi-track, which have stricter procedures and higher potential costs.

Judgments Against Businesses

Small‑claims judgments can be entered against individuals or limited companies. If the defendant is a business, the court can order an officer of the company to attend court to provide information about its finances. This helps you decide whether to use wage deductions (if the debtor is an employee) or property charges (if the company owns assets).

Step 2: Waiting for Payment or Negotiating an Agreement

After the judgment, the debtor normally has 14 days to pay. If the order specifies a different time frame, follow that. Legal commentary notes that “if the court doesn’t specify a deadline, the standard timeframe is 14 days from the judgment date”. During this period, the debtor may:

- Pay in full. Always provide clear payment instructions and confirm receipt.

- Propose instalments. They might ask to spread payments over time. You can accept, negotiate or ask the court to vary the order if you believe the offer is unreasonable.

- Ignore the order. If you receive no payment or contact after 14 days, you can begin enforcement.

It’s good practice to send a polite reminder soon after judgment. Keep written records of all correspondence, calls and payments. If you agree to instalments privately, put the agreement in writing and update the court only if you wish to formalise the arrangement. CaseCraft.AI provides secure messaging and document storage that makes record‑keeping easier. The platform also alerts you when payment deadlines expire so you can take the next step without delay.

If you haven’t yet filed a claim, read our guide on how to file a small claim online to understand the pre‑action requirements.

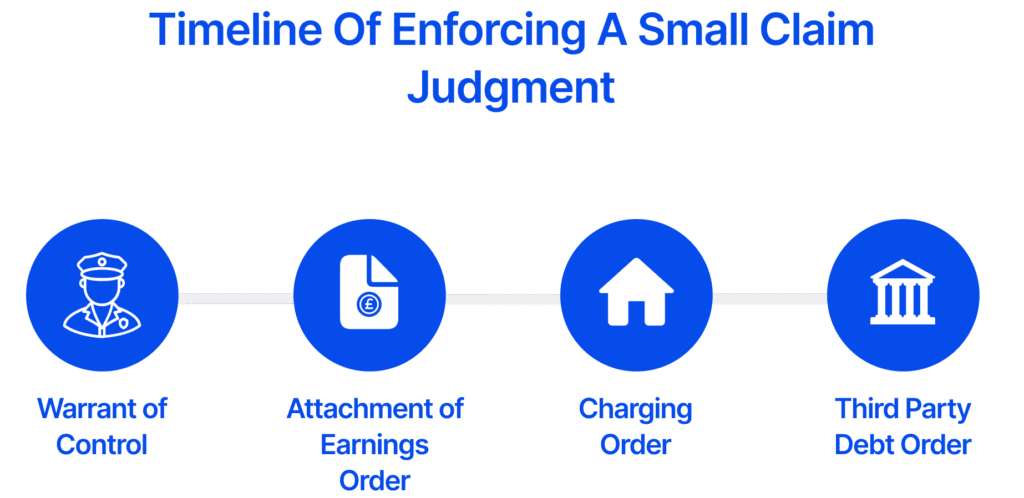

Step 3: Enforcing the Judgment

If the debtor fails to pay voluntarily, you can ask the court to enforce the judgment. This process is known as enforcing a County Court Judgment (CCJ). You’ll need to pay a small fee, which can usually be recovered from the debtor, and then choose the right enforcement tool based on their financial circumstances. Below are the main options.

For step-by-step help choosing and using the right method, read our Small Claims Enforcement Guide.

Warrant of Control (County Court Bailiffs)

A warrant of control authorises county court bailiffs (now called enforcement agents) to seize and sell the debtor’s goods. After you apply, the bailiff sends a notice giving at least 7 days’ warning. If the debt remains unpaid after the notice, the bailiff can visit between 6 am and 9 pm, take control of non‑essential items and sell them at auction. Essential household goods and items required for work cannot be taken. You can apply to either a county court or the High Court if you’re owed between £600 and £5,000; above this amount, you can request a writ of control in the High Court. The application fee is £94 from April 2025.

Eligibility and forms: You can apply for a warrant of control using form N323 (county court) or transfer the CCJ to the High Court using form N293A (judgment must be at least £600). The bailiff will ask the debtor to pay within seven days, then visit if necessary.

High Court Writ of Control

If your judgment is over £600, you can transfer it to the High Court for faster enforcement. High Court Enforcement Officers (HCEOs) have broader powers and often achieve higher recovery rates. To do this, you apply for a writ of control, paying a sealing fee of £80. HCEOs can act nationwide and may charge additional enforcement fees, but these are usually added to the debt and recovered from the debtor. High Court action is ideal for larger claims or stubborn debtors.

Attachment of Earnings Order

When the debtor is an employee, the court can instruct their employer to deduct money from their wages. This attachment of earnings order is sent directly to the employer. The creditor cannot apply for an attachment of earnings order if the debtor owes less than £50 or is self‑employed, unemployed or serving in the armed forces. The court decides the deduction amount, ensuring the debtor has enough to live on. An application for an attachment of earnings order costs £135. It is a good option when the debtor has a steady job.

Charging Order and Order for Sale

A charging order secures the debt against the debtor’s property (usually their home). Once a CCJ is obtained, you can apply for an interim charging order using form N379. If granted, the charge is registered with HM Land Registry. This prevents the property from being sold or refinanced without settling your debt. The application fee for a charging order is £135. Note that a charging order does not automatically force a sale; to realise the debt, you may need to apply for an order for sale, which is a separate process often reserved for high‑value debts. Charging orders are useful when the debtor owns significant equity but lacks cash.

Third‑Party Debt Order

If you know the debtor has funds in a bank or building society account, you can ask the court to freeze and seize those funds. A third‑party debt order requires the bank to hold the money and, following a court hearing, release it to you. The process involves an interim order to freeze the account and a final hearing at least 28 days later to decide whether the money should be paid to the creditor. The application fee is £135.

In Order to Obtain Information

If you’re unsure about the debtor’s assets or income, you can ask the court to order them (or, for companies, an officer) to attend and provide financial information. This is often called an order to obtain information or “a questioning order”. The hearing is an opportunity to ask under oath about employment, bank accounts and property. Fees start at £67. The information you obtain can help you decide which enforcement method is likely to succeed.

Combining Enforcement Methods

Under the Civil Procedure Rules, a judgment creditor can use more than one enforcement tool at the same time. For example, you might obtain an attachment of earnings order while simultaneously placing a charging order on the debtor’s home. Combining methods increases the chance of recovery and signals to the debtor that you are serious. CaseCraft.AI guides users through this process and auto‑generates the necessary forms.

Step 4: Calculating Interest and Enforcement Costs

Statutory Interest

Unless your contract specifies a different rate, judgments attract statutory interest of 8 % per year under the County Courts Act 1984. To work out interest on a fixed amount, multiply the debt by 0.08 to get the annual interest and divide by 365 for a daily rate. Interest starts from the date of judgment and continues until payment is received. This table illustrates how interest accrues:

| Claim amount | Annual interest (8 %) | Six‑month example |

| £1,000 | £80 | £40 |

| £5,000 | £400 | £200 |

| £10,000 | £800 | £400 |

In addition to statutory interest, you can claim your enforcement costs. Court fees for warrants, attachment orders and charging orders (outlined above) are added to the debt. Bailiffs and high court enforcement officers charge fees regulated by the Taking Control of Goods (Fees) Regulations 2014, and these can also be recovered. Keep receipts of all expenses so you can demonstrate them to the court.

Cost‑Benefit Analysis

Before applying for enforcement, consider whether the debtor has assets or income to cover both the principal and the additional costs. If the debtor is insolvent or unemployed, a warrant of control may fail, and you could lose your fee. CaseCraft.AI helps claimants assess the debtor’s situation and suggests the most cost‑effective enforcement option based on information gathered during the claim.

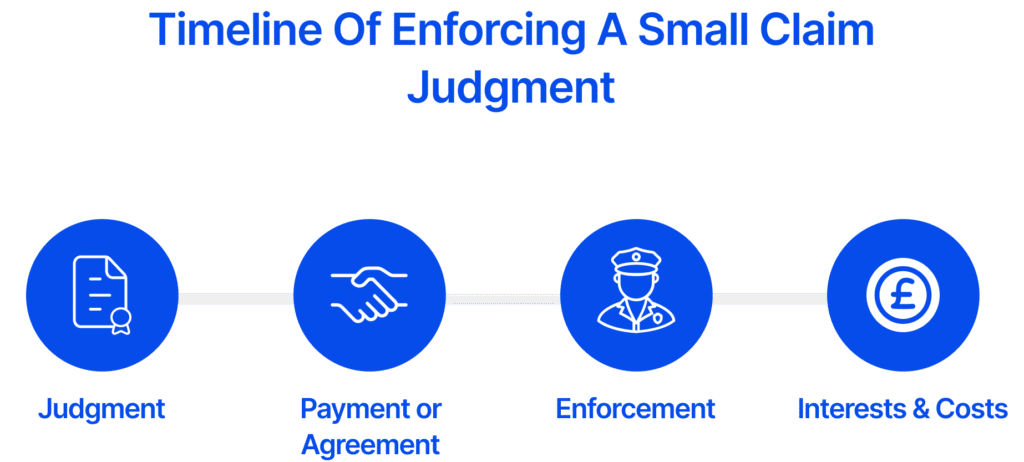

The timeline above summarises the typical stages: judgment issued, 14‑day payment period, choose enforcement, interest accrues, and judgment satisfied.

Step 5: What if the Defendant Still Does not Pay?

Judgments remain enforceable for six years from the date they become payable. You can attempt enforcement at any point during this period, and even reapply for different methods if circumstances change (for example, the debtor gets a job or sells a property). However, after six years, you must ask the court for permission to enforce. The court will only grant permission if there are exceptional circumstances and it is “demonstrably just” to do so. Delay can reduce your chances of recovery because interest on a judgment is recoverable only for six years, and the debtor may hide or dissipate assets.

If enforcement fails repeatedly, consider whether insolvency proceedings (bankruptcy for individuals or winding‑up for companies) may be appropriate. These routes are beyond the small‑claims process and involve separate legal steps and fees.

Step 6: Marking the Judgment as Satisfied

Once the debtor pays in full, you should inform the court so the CCJ enforcement process can be marked as satisfied. Paying the judgment within one month allows the record to be removed from the Register of Judgments. Payments made after one month remain on the register for six years but show as satisfied. To update the record, you submit form N443 and pay a small fee (£19 as of April 2025). You should provide proof of payment, such as bank statements, when requesting the update. The court then notifies the credit reference agencies. Maintaining accurate records protects both parties’ credit histories.

Step 7: Tax and Accounting Considerations

For individuals recovering personal debts, the money you receive after enforcing a small claim generally isn’t taxable because you are simply getting back what you are owed. However, businesses recovering unpaid invoices must treat the amounts as income. If you previously wrote off the invoice as a bad debt, you may need to reverse the bad‑debt relief in your accounts when you receive payment. Interest and costs recovered could also be taxable income. Always consult an accountant if the sums are significant or your business uses accrual accounting.

Step 8: Preventing Future Payment Issues

Winning a small claim and enforcing it can be time‑consuming and stressful. To reduce the risk of non‑payment in future:

- Use clear written contracts. Always document the terms of your agreement, small claims payment deadlines and penalties for late payment. If you trade on credit, consider setting out interest rates and enforcement costs in your terms and conditions.

- Perform basic due diligence. Check a customer’s credit record, trading history and ability to pay before extending credit.

- Secure deposits or guarantees. Taking a deposit or personal guarantee reduces the risk of default.

- Use structured payment schedules. For large projects, request staged payments instead of waiting for a single invoice.

- Use digital tools. CaseCraft.AI offers a secure platform to file, manage and enforce small claims. It guides you through form completion, stores correspondence, calculates interest automatically and integrates with HMCTS systems. Because it is designed specifically for small claims within the monetary limits, it ensures compliance with court rules and prevents mistakes.

For guidance on collecting and presenting evidence, see what counts as evidence.

Take Control of Your Judgment

Winning in small claims court is only the first step towards recovering your money. You must understand the small claim enforcement UK process, decide whether to use bailiffs, wage deductions, property charges or other enforcement methods, and track interest and costs. Acting promptly within the six-year enforcement window and keeping clear records maximise your chances of recovering money owed after judgment. Tools like CaseCraft.AI simplify this journey by guiding you through each stage, generating court forms automatically and providing a secure hub for your evidence. Use this guide as your roadmap to enforce your small claims court judgment in the UK, collect what you are owed, and move forward with confidence.

Note: This information is accurate as of November 2025. Court fees and procedures may change. Always check GOV.UK for the latest information. This article is for general information purposes only and does not constitute legal advice. You should seek independent legal guidance or consult a qualified solicitor before taking any action related to court enforcement or small claims.

FAQ: Winning a Small Claim (2025)

How long does it take to get paid after winning a small claim?

Payment isn’t instant. The debtor usually has 14 days to comply. If they pay within 30 days, the CCJ can be removed from the register. If they ignore the order, you must apply for enforcement. Simple cases enforced through bailiffs or attachment of earnings often resolve within a few months, but complex cases can take longer, especially if the debtor disputes enforcement or lacks assets.

What if the defendant refuses to pay after a CCJ?

You can choose from several enforcement options after judgement: bailiffs (warrant of control), high court writs, attachment of earnings orders, charging orders and third‑party debt orders. The method you choose depends on the debtor’s assets, employment status and the debt value. Remember to add enforcement costs and statutory interest to the amount owed.

Can I send bailiffs after winning a small claim?

Yes. After the 14‑day payment period expires, you can apply for a warrant of control. The bailiff gives at least 7 days’ notice, and can visit between 6 am and 9 pm to take non‑essential goods. For debts over £600, you can transfer the judgment to the High Court for a writ of control.

Do I need to go back to court to enforce a judgment?

You don’t need another hearing to start enforcement. You complete the relevant application form (e.g., N323 for a warrant of control, N337 for an attachment of earnings order, N379 for a charging order) and pay the fee. The court reviews the application administratively and issues the order. If the debtor challenges enforcement, a hearing may be scheduled.